A Timeline of Wealth Inequality in the United States

Foundations of Modern Wealth Inequality (1990-2000)

The beginning of the Federal Reserve’s Distributional Financial Accounts dataset marks a decade in which context is provided for aspects in our research question: the change in the relationship between education and household wealth. Specifically referring to the 1990s, higher education was determined to be a reliable source of upwards mobility and wealth attainment due to several factors. However, to explain these factors requires an understanding of the fiscal structure left behind as an effect of the Reagan-era tax reforms.

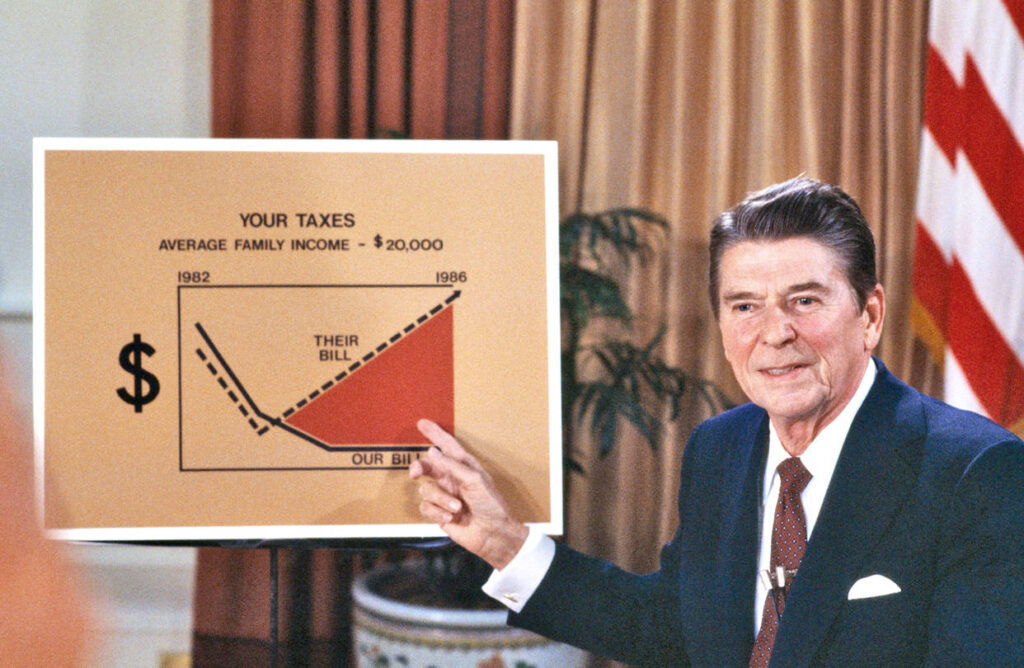

1980s Tax Reform

The 1980s as a precursor to the 1990s saw two major tax reform acts; the Tax Reform Act of 1986 and the Economic Recovery Tax Act (ERTA) of 1981. The effect of the Tax Reform Act of 1986 was the decrease in the tax rate for those who earned the top marginal income to 28%, thus creating a pathway for those with already high income to widen the gap. The Economic Recovery Tax Act of 1981 lowered the tax rate for capital gains to 20% in an attempt to encourage investment in business and boost the stock market, but mainly increased the value of capital for those who already possessed assets. These policies essentially empowered capital owners, with a steeper benefit only capable of being seen with more long term possession of these assets (Saez and Zucman). However, the immediate effects of these tax reforms in the decade of the 1990s are often overshadowed by the strong economic growth in educated workers.

The economic expansion seen in the 1990s was characterized by the birth of the commercial internet, college enrollment expansion, and expansion in mortgage and credit. The overall increase in wages and imbalance of power between educated workers and low-skill workers; known as “the skills premium”, saw the Telecommunications Act of 1996 as a huge factor, driving the workforce towards those trained in STEM and business fields. Under this law, the telecommunications industry was deregulated and as a result, the dot-com boom rose with several software, hardware, telecom, and internet companies, all demanding high skilled labor and technical degrees. Hubmer in Sources of US Wealth Inequality: Past, Present, and Future notes that, “since at least 1992, it has been well-documented that the education skill premium has risen” (Hubmer et al. 393).

Education Attainability

Coupling the increase in demand for workers in the tech industry with the sudden expansion of availability to college had, within the decade, provided short term benefit to a sudden growth in wages, and a pathway to attain them, but had also simultaneously set the groundwork for financial ruin for many as time progressed. The Higher Education Act Reauthorization of 1992 created the Unsubsidized Stafford Loan, granting the ability to all students, regardless of financial background, to take out massive amounts of loans. It also expanded Pell Grant coverage, but did not adjust to the rising cost of tuition as time progressed. The stagnant wages for low-skilled labor created early dependency of low-income to middle-class on loans to attain the very education that qualified one for high wage professions. In The Role of Higher Education in Social Mobility, Robert Haveman and Timothy Smeeding acknowledge that, “access to higher education during this period remained heavily stratified by family income: students from the wealthiest quartile of households still received nearly half of all higher-education resources, while students from the bottom quartile received only 7 percent” (Haveman and Smeeding 131–132). This implies an imbalance in the long-term wealth accumulation benefit for attaining a Bachelor’s degree, in which the outcome was still largely dependent upon family income/background. To elaborate further upon this family income/background dependency, Florencia Torche in Is a College Degree Still the Great Equalizer pays a large amount of detail to what is acknowledged as a plateau in the effects of attaining a Bachelor’s Degree, where pursuing higher education both at the Bachelor’s and Master’s levels had benefits exponentiated as a factor of privileged networks and inherited wealth (Torche).

Credit and Mortgage Expansion

The dependency of mobility on borrowing also extended to the expansion of mortgages and consumer credit, particularly for income groups without a sufficient amount of savings. Two major legislations were passed during this decade that directly contributed to this; the Federal Housing Enterprises Financial Safety and Soundness Act of 1992 and the Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994. An effect of the Federal Housing Enterprises Financial Safety and Soundness Act of 1992 was the sudden increase in mortgage credit availability for low and moderate income borrowers, while the Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994 enabled banking operations on the national scale and encouraged aggressive consumer lending also to that degree. For higher education and home ownership; two critical factors in securing base income and upward mobility at the time, this further enabled the dependency on loans. In “Credit Constraints and Demand for Higher Education: Evidence from Financial Deregulation” The Review of Economics and Statistics, Stephen Tang and Constantine Yannelis showed that despite deregulation of credit markets expanding loan accessibility and college enrollments for lower and middle income families, the dependence on debt became apparent and exponential in order to obtain upward mobility (Sun and Yannelis). The unprecedented financial risk undertaken by the spike in mortgage lending and consumer credit painted the foundation for huge economic crises that occurred within the later decades; the 2008 housing crash and the ongoing student-debt crisis.

Conclusion of Pre-2000’s Context

The combination of the demand for skilled workers upon the expansion of new industries in the United States Economy, wage growth for said skilled workers, and growing accessibility to higher education, mortgage, and consumer credit through the free distribution of loans created what some may call the “illusion of wealth mobility” in the 1990s. The illusion being that the economic structure set in place by the 1980s actually caused households already possessing huge sums of financial assets to experience a compounded wealth growth, thereby widening the wealth gap, as opposed to the initial wealth growth from the rising wages rewarded to those with higher education at the time. Yonatan Berman in Modeling the Origin and Possible Control of the Wealth Inequality Surge describes this particular decade as the time in which the effects of a “capital-dominated” economy were beginning to be seen, where investment returns posed the core driver for wealth inequality on a scale that even the rise in wages from education could not close.

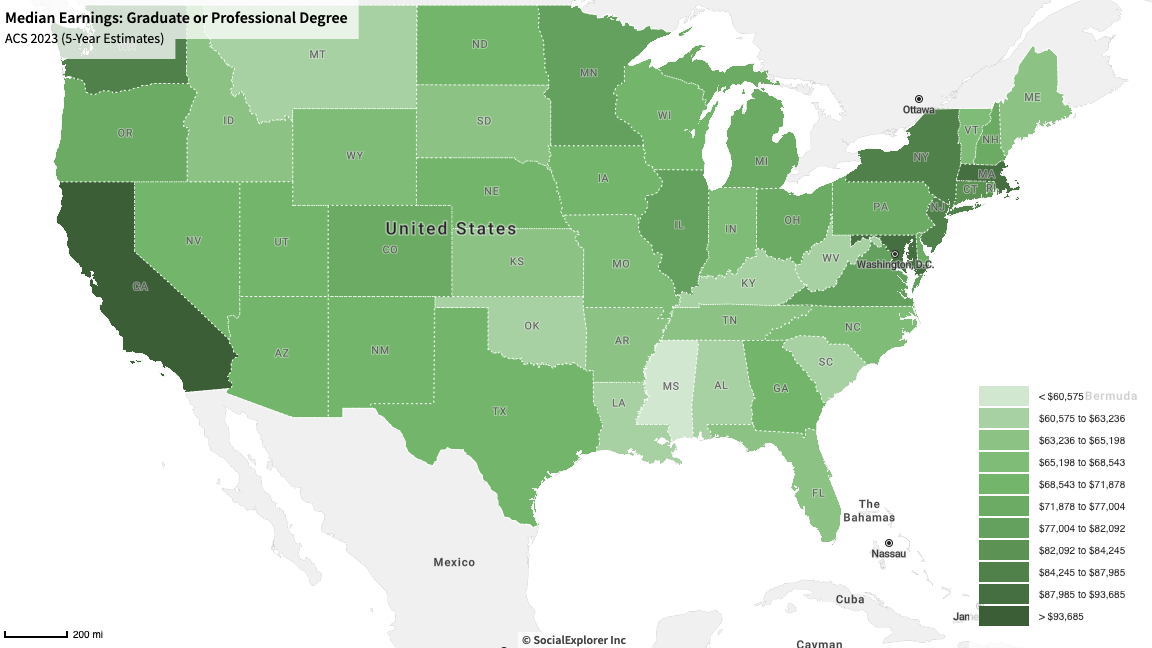

Geographical Context

This map is a nationwide representation, state by state, of a data set pertaining to the American Community Survey conducted by the United States Census Bureau. It was created through Social Explorer and tracks the median earnings for individuals with a graduate or professional degree, with darker shading across different states representing a higher median in earnings. This was chosen as a representation towards the narrative that explains the wealth gap and how those who achieve higher education are affected in terms of upward mobility. Relevant to our data set is the actual income of those with higher education. Seeing first whether the standard earnings of those with a professional degree contains a level of income that can close the wealth gap little by little, and then seeing whether higher education directly correlates with reaching a relatively high income, is essentially part of the answer to our group’s research question.

According to the map, the areas with a large concentration of high median salary are states along the coast line (West Coast: California, Washington, East Coast: New York, Massachusetts). In contrast, almost every state in the Mid West or South has low to mid-range earnings for those with higher education. This at the very least suggests geographical factors, in which states with longer established industries or industries that require higher education, i.e. healthcare, tend to either have a larger population of those with higher education or can offer a higher standard of living for them. Age and generational wealth are shown to be the major factors for the wealth gap data that we provided, but regional economic access as well as urban-rural economic divides account for cost of living adjustments centered on locations that hold the majority of the nation’s wealth. It may imply that education needs to be coupled with place-based opportunity to make any real progress towards closing the wealth gap.